UNITED STATES, Plaintiff, v. EVELYN SOLOMON, by and through her Guardian Julia Solomon, Defendant.

Subsequent History: Motion denied by, Motion denied by, As moot United States v. Solomon, 2021 U.S. Dist. LEXIS 214940 (S.D. Fla., Nov. 1, 2021)

Counsel: 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1For United States, Plaintiff: John P. Nasta, LEAD ATTORNEY, U.S. Department of Justice, Washington, DC USA.

For Evelyn Solomon, by and through her Guardian Julia Solomon, Defendant: Joseph Andrew DiRuzzo, III, LEAD ATTORNEY, Daniel Lader, DiRuzzo & Company, Ft. Lauderdale, FL USA.

Judges: AILEEN M. CANNON, UNITED STATES DISTRICT JUDGE.

570 F. Supp. 3d 1195 2021 U.S. Dist.

LEXIS 210602 2021 WL 5001911 at 1197 ORDER

DENYING DEFENDANT'S MOTION FOR PARTIAL SUMMARY JUDGMENT [ECF No. 11] AND

GRANTING PLAINTIFF'S CROSSMOTION FOR PARTIAL SUMMARY JUDGMENT [ECF No. 18]

THIS CAUSE comes before the Court upon Defendant's Motion for Partial Summary Judgment (the "Motion") [ECF No. 11] and Plaintiff's Cross-Motion for Partial Summary Judgment (the "Cross-Motion") [ECF No. 19]. The Court has reviewed the Motion, the Cross-Motion, and the full record [ECF Nos. 10, 18, 19, 31, 32, 37]. Upon careful review, Defendant's Motion for Partial Summary Judgment is DENIED, and Plaintiff's Cross-Motion for Partial Summary Judgment is GRANTED.

FACTUAL BACKGROUND

1

The following facts are drawn from Solomon's Statement of Material Facts [ECF No. 10], the Government's Response to Solomon's Statement of Material Facts [ECF No. 18], and Solomon's Combined Response/Reply Statement of Material Facts [ECF No. 31].

This is an action brought by the United States ("Government" or "United States") to enforce non-willful civil penalties assessed against Defendant Evelyn Solomon ("Solomon" or "Defendant") for failing to timely report her570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 2 financial interest in foreign bank accounts, as required by the Bank Secrecy Act ("BSA"), 31 U.S.C. § 5311, et seq., and implementing regulations.

The following facts are undisputed. Solomon is a United States Citizen and resides in Florida. During the 2004-2010 tax years, Solomon had access to several foreign bank accounts, but she did not report those accounts to the Internal Revenue Service ("IRS") as required by law [ECF No. 10 ¶ 1; ECF No. 18-3; ECF No. 18 ¶¶ 26, 28; ECF No. 31 ¶¶ 26, 28]. Specifically, Solomon did not file a "Report of Foreign Bank and Financial Accounts" form, commonly known as an "FBAR," for tax years 2004-2010 [ECF No. 18 ¶ 26; ECF No. 31 ¶ 26]. On March 13, 2012, however, as part of the IRS's 2012 Offshore Voluntary Disclosure Program ("OVDP"), Solomon filed FBARs for 2004-2010, voluntarily disclosing her financial interest in multiple bank accounts during those years [ECF No. 18 ¶¶ 27-29; ECF No. 31 ¶¶ 27-29].

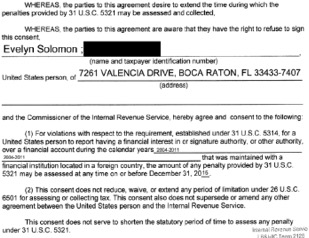

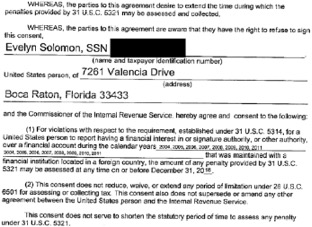

The statute of limitations to assess penalties for violating 31 U.S.C. § 5314 is six years [ECF No. 10 ¶ 2; ECF No. 18 ¶ 2]. As relevant here, however, Solomon signed two consent agreements, each entitled "Consent to Extend the Time to Assess Civil Penalties Provided by 31 U.S.C. § 5314 for FBAR Violations" [ECF No. 10-1; ECF No. 10-2].570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 3 Solomon signed the first consent agreement on August 26, 2013, stating that, for violations of 31 U.S.C. § 5314 during the years "2004-2011," penalties provided by 31 U.S.C. § 5321 "may be assessed at any time on or before December 31, 2015" [ECF No. 10-1]. On February 10, 2017, Solomon signed a second 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1198 agreement, this time listing out the years individually: "2004, 2005, 2006, 2007, 2008, 2009, 2010, 2011" [ECF No. 10-2]. This second agreement states that, for violations of 31 U.S.C. § 5314 during those years, penalties under 31 U.S.C. § 5321 "may be assessed at any time on or before December 31, 2018" [ECF No. 10-2]. Pertinent portions of both forms are pictured below [ECF Nos. 10-1 and 10-2], and both forms are followed by a signature block with dated, handwritten signatures from Solomon and a designated IRS representative:

570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1199

On November 17, 2018, after Solomon signed both consent forms, Solomon signed an IRS Form 13449 document entitled "Agreement to Assessment and Collection of Penalties" [ECF No. 18 ¶ 31; ECF No. 31 ¶ 31]. Solomon's attorney at the time also signed the form on November 19, 2018 [ECF No. 18 ¶ 32; ECF No. 31 ¶ 32]. The form states the following above the signature line: "I consent to the immediate 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 4 assessment and collection of the penalty amount specified above," and then it lists $200,000 as the "TOTAL proposed penalty" [ECF No. 18-3 p. 1]. In the following pages of the form, under the heading "Foreign Account Penalty Information," the form itemizes that $200,000 total, listing twenty separate $10,000 penalties, each associated with a particular foreign bank account/institution/agent listed on the form, corresponding to the calendar years 2004-2010 [ECF No. 18-3 pp. 2-4].

2

The signed Form 13449 lists out the foreign accounts one by one and contains boxes to fill in the particular foreign account number and/or foreign agent and the maximum value of funds in that account for the calendar year listed [ECF No. 18-3].

On December 12, 2018, the IRS assessed penalties against Solomon in the total amount of $200,000—specifically, $10,000 penalty for each of the twenty unreported foreign bank accounts during the years 2004-2010 [ECF No. 18 ¶ 33; ECF No. 31 ¶ 32].

PROCEDURAL HISTORY

On December 9, 2020, the United States filed a single-count complaint against Solomon seeking a judgment for non-willful penalties under 31 U.S.C. § 5321 in the amount of $226,657.54 as of November 6, 2020, plus penalties and interest that continue to accrue [ECF No. 1 pp. 5-7].

On February 1, 2021, Solomon moved for partial summary judgment seeking to reduce the penalty to $70,000 [ECF No. 11 p. 17]. Solomon argues that the penalty 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1200 assessed against her should be partially 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 5 time barred as to the penalties for violations in 2004-2009 [ECF No. 11 pp. 4-11]. Solomon also argues that non-willful violations of 31 U.S.C. § 5314 should be assessed on a per-form rather than on a per-account basis, thereby reducing the number of violations and the corresponding total penalty from approximately $200,000 to $70,000 (not including interest) [ECF No. 11 pp. 11-17].

On February 16, 2021, the Government responded to Solomon's Motion and cross-moved for partial summary judgment [ECF No. 19]. The Government argues that the six-year statute of limitations in 21 U.S.C. § 5321(b)(1) is non-jurisdictional in nature and therefore waivable, and that Solomon clearly and knowingly waived the limitations period by consenting to the extension agreements referenced above. As for the total amount of the penalty assessed ($70,000 versus $200,000), the Government asserts that, based on the plain text and structure of the Bank Secrecy Act and implementing regulations, see 31 U.S.C. §§ 5314(a), 5321(a)(5)(A)-(B); 31 C.F.R. §§ 1010.350, 1010.306, it properly assessed the penalty using a per-account basis rather than on a per-form basis [ECF No. 19 pp. 3-15]. The Motion and Crossmotion are both ripe for adjudication.

LEGAL STANDARD

Summary judgment is appropriate where there is "no genuine issue as to any 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 6 material fact [such] that the moving party is entitled to judgment as a matter of law." Celotex Corp. v. Catrett, 477 U.S. 317, 322, 106 S. Ct. 2548, 91 L. Ed. 2d 265 (1986); Fed R. Civ. P. 56(a). An issue of fact is "material" if it might affect the outcome of the case under the governing law. See Anderson v. Liberty Lobby, Inc., 477 U.S. 242, 248, 106 S. Ct. 2505, 91 L. Ed. 2d 202 (1986). It is "genuine" if the evidence could lead a reasonable jury to find for the non-moving party. See id.; see also Matsushita Elec. Indus. Co. v. Zenith Radio Corp., 475 U.S. 574, 587, 106 S. Ct. 1348, 89 L. Ed. 2d 538 (1986). At summary judgment, the moving party has the burden of proving the absence of a genuine issue of material fact. See Allen v. Tyson Foods Inc., 121 F.3d 642, 646 (11th Cir. 1997). The non-moving party's presentation of a "mere existence of a scintilla of evidence" in support of its position is insufficient to overcome summary judgment. Anderson, 477 U.S. at 252.

"For factual issues to be considered genuine, they must have a real basis in the record." Mann v. Taser Int'l, Inc., 588 F.3d 1291, 1303 (11th Cir. 2009) (internal quotation marks omitted). Speculation or conjecture cannot create a genuine issue of material fact. Cordoba v. Dillard's, Inc., 419 F.3d 1169, 1181 (11th Cir. 2005). The moving party has the initial burden of showing the absence of a genuine issue as to any material fact. Clark v. Coats & Clark, Inc., 929 F.2d 604, 608 (11th Cir. 1991). In assessing whether the moving party has met this burden, the court must view the movant's evidence and all factual inferences arising from it in the light most favorable to the non-moving party. Denney v. City of Albany, 247 F.3d 1172, 1181 (11th Cir. 2001). Once the moving party satisfies its initial burden, the burden shifts to the non-moving party to come570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 7 forward with evidence showing a genuine issue of material fact that precludes summary judgment. Bailey v. Allgas, Inc., 284 F.3d 1237, 1243 (11th Cir. 2002); Fed. R. Civ. P. 56(e).

DISCUSSION

A. Statute of Limitations

The Court first considers Solomon's argument that the $200,000 penalty assessed against her for FBAR violations in years 2004-2010 is partially time barred as to all 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1201 but year 2010. The answer is no; Solomon clearly and unambiguously waived any statute of limitations defense by consenting to an extension of the time provided to assess civil penalties under 31 U.S.C. § 5321.

The Bank Secrecy Act provides as follows: "The Secretary of the Treasury may assess a civil penalty [for violations of 31 U.S.C. § 5314] at any time before the end of the 6-year period beginning on the date of the transaction with respect to which the penalty is assessed." 31 U.S.C. § 5321(b)(1). There is no dispute that the application limitations period is six years [ECF No. 10 ¶ 2; ECF No. 18 ¶ 2].

Solomon contends that, by the time she signed the first consent form on August 26, 2013, the limitations period for tax years 2004-2006 already had expired [ECF No. 11 p. 8; ECF No. 10-1]. As for years 2007-2009, Solomon argues that, although the first waiver extended the limitations period for those years until December 31, 2015, such period had expired570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 8 by the time she signed the second waiver on February 10, 2017 [ECF No 11 p. 8; ECF No. 10-2]. In other words, according to Solomon, the waivers she signed did not have the effect of extending the limitations period because, by the time she signed them, the limitations period covering her conduct had expired—leaving nothing to waive. Solomon additionally argues that, even if she could have waived the limitations period, she did not knowingly or unambiguously do so as to the years where the limitations period had expired (referring to 2004-2009) [ECF No. 32 pp. 6-13]. She then suggests that her former attorney (the attorney who represented her at the time she signed the forms) potentially could show, through evidence not currently in the record, that Solomon did not agree to extend the expired limitations period, and she asks for an opportunity to conduct discovery to determine what her former counsel knew about her intent regarding the waiver forms [ECF No. 32 pp. 13-15; see ECF No. 44].

The Government responds that the statute of limitation in 31 U.S.C. § 5321(b)(1) is a non-jurisdictional defense that can be waived, even after it expires, and that Solomon did so here—signing a consent form that explicitly570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 9 and unambiguously consented to extending the time to assess applicable penalties for FBAR violations until December 31, 2018 [ECF No. 37 pp. 4-10; ECF No. 19 pp. 8-10].

The Court agrees with the Government that the applicable statute of limitations, 31 U.S.C. §5321, is a waivable defense that can be waived even after it has expired. The key inquiry in determining if a limitations period can be waived is "whether it limits courts' subject matter jurisdiction—in which case its time bar is not waivable—or is instead a non-jurisdictional claim-processing rule—in which case waiver is permissible." Sec., U.S. Dept. of Lab. v. Preston, 873 F.3d 877, 881 (11th Cir. 2017) (citing In re Pugh, 158 F.3d 530, 543 (11th Cir. 1998)).

It is clear from the face of the limitations period in Section 5321(b)(1)—which does not refer to the Court's jurisdiction in any respect—that it operates merely as an affirmative defense, not as a limit or condition on the Court's jurisdiction. See 31 U.S.C. § 5321(b)(1) ("The Secretary of the Treasury may assess a civil penalty under subsection (a) at any time before the end of the 6-year period beginning on the date of the transaction with respect to which the penalty is assessed."). Because 31 U.S.C. § 5321 is not jurisdictional, the limitations period for assessing FBAR penalties may be waived by the parties, even for claims that have expired. See United States v. Hitachi Am., Ltd., 172 F.3d 1319, 1334 (Fed. Cir. 1999) ("[I]f [a statute]570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 10 is not jurisdictional, then as merely an affirmative defense, the statute 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1202 of limitations can be waived by the parties even for claims that have expired." (citing authorities)); United States v. Schwarzbaum, 18-CV-81147, 2019 U.S. Dist. LEXIS 143348, 2019 WL 3997132, at *4 (S.D. Fla. Aug. 23, 2019) (finding limitations period for assessing FBAR penalties under 31 U.S.C. § 5321 could be properly extended by agreement).

The Court also rejects Solomon's argument that she did not knowingly waive the limitations period when she signed the relevant consent agreements [ECF No. 10-1; ECF No. 10-2]. The second consent agreement, signed by Solomon on February 10, 2017, states in explicit terms—without reservation or limitation—that penalties for violations under 31 U.S.C. § 5314 for the specifically listed calendar years of 2004, 2005, 2006, 2007, 2008, 2009, 2010, 2011 may be assessed at any time before December 31, 2018 [ECF No. 10-2]. This language is clear, unambiguous, and unlimited, and no additional discovery is warranted to shed light on that clear waiver [ECF No. 10-2 ("[T]he amount of any penalty provided by 31 U.S.C. 5321 may be assessed at any time on or before December 31, 2018." (emphases added))]. Indeed, the form explicitly references, in list form, the specific years that were being extended: "2004, 2005, 2006, 2007, 2008, 2009, 2010, 2011"570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 11 [ECF No. 10-2]. There is no dispute that Solomon signed the form, which is clearly entitled "Consent to Extend the Time to Assess Civil Penalties Provided by 31 U.S.C. § 5321 for FBAR Violations" [ECF No. 10-2].

3

Also worth noting is that, approximately one month before the IRS assessed penalties for those specific years (2004-2011), Solomon and her attorney signed the IRS Form 13449—"Agreement to Assessment and Collection of Penalties Under 31 U.S.C. § 5321(a)(5) and 5321(a)(6)"—which itself goes through those calendar years, listing penalties and foreign accounts, ultimately yielding a total penalty for the specific years as to which she waived a limitations defense [ECF No. 18-3 p. 4].

Based on this clear record evidence, Solomon knowingly and voluntarily waived the period of limitations for assessing FBAR penalties as to the tax years 2004-2011 until December 31, 2018. The government's Cross-Motion is granted as to the statute of limitations.

B. FBAR Penalties Apply on a Per-Account

rather than Per-Form Basis

The Court next considers whether the penalty for a non-willful violation of 31 U.S.C. § 5314 applies on a per-account (referring to individual bank accounts maintained during a calendar year) or on a per-form basis (referring to the FBAR form itself). This presents a question of statutory and regulatory interpretation so far not addressed by the Eleventh Circuit.

4

Of the courts that have addressed this issue to date, all but one have rejected the government's view, ruling or otherwise suggesting that a non-willful "violation" of the reporting requirement in 31 U.S.C. § 5314 is the failure to file an annual FBAR report—not the failure to "report" the citizen's interest in each foreign financial account. See United States v. Boyd, 991 F.3d 1077 (9th Cir. 2021) (rejecting government's view); United States v. Bittner, 469 F. Supp. 3d 709 (E.D. Tex. 2020) appeal docketed, No. 20-40612 (5th Cir. Sept. 18, 2020) (same); United States v. Kaufman, 3:18-CV-00787 (KAD), 2021 U.S. Dist. LEXIS 4602, 2021 WL 83478, **8-11 (D. Conn. Jan. 11, 2021) (same); United States v. Giraldi, CV202830SDWLDW, 2021 U.S. Dist. LEXIS 49481, 2021 WL 1016215, *5 n.8 (D.N.J. Mar. 16, 2021) (same). But See United States v. Stromme, 2021 U.S. Dist. LEXIS 21498, No. 20-24800-CIV (S.D. Fla. Jan. 25, 2021) (ECF No. 18 p. 3) (granting judgment in favor of United States for the full amount of penalties sought, agreeing that "each unreported relationship with a foreign financial agency constitutes an FBAR violation").

1. Statutory and Regulatory Framework

The IRS assessed civil penalties against Solomon under 31 U.S.C. § 5321(a)(5). 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1203 That statute permits the Secretary of the Treasury to "impose a civil money penalty on any person who violates, or causes any violation of, any provision of section 5314." 31 U.S.C. § (a)(5).

5

The Bank Secrecy Act caps the amount of a penalty for a non-willful violation at $10,000. 31 U.S.C. § 5321(a)(5)(B)(i) ("[T]he amount of any civil penalty imposed [for a non-willful violation] . . . shall not exceed $10,000."). Further, pursuant to the so-called "reasonable cause exception," "[n]o penalty shall be imposed" for a non-willful penalty if—(I) such violation was due to reasonable cause, and (II) the amount of the transaction or the balance in the account at the time of the transaction was properly reported." 31 U.S.C. § 5321(5)(B)(ii).

The statute does not570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 12 further define the term "violation."

As relevant here, 31 U.S.C. § 5314 directs the Secretary to require United States citizens or residents "to keep records, file reports, or keep records and file reports, when the resident, citizen, or person makes a transaction or maintains a relation for any person with a foreign financial agency." 31 U.S.C. § 5314(a). Section 5314 then mandates that "[t]he records and reports" contain certain information as prescribed by the Secretary, including "the identity and address of participants in a transaction or relationship," id. § 5314(a)(1), "the identity of real parties in interest," id. § 5314(a)(3), and "a description of the transaction," id. § 5314(a)(4).

The Secretary of the Treasury has implemented regulations to carry out the recording and reporting directive in Section 5314. Those regulations are principally contained in Title 31, Part 1010, Subpart C of the Code of Federal Regulations (Reports Required to be Made),

6

Subpart D also contains a relevant provision entitled "Records to be Made and Retained by Persons Having Financial Interests in Foreign Financial Accounts." 31 C.F.R. § 1010.420.

and two are relevant here.

7

See 31 C.F.R. §§ 1010.300, 1010.301, 1010.306, 1010.310, 1010.311, 1010.312, 1010.313, 1010.314, 1010.315, 1010.320, 1010.330, 1010.331, 1010.340, 1010.350, 110.360, 1010.370.

The first derives from Section 1010.350, entitled "Reports of foreign financial accounts," and its main provision is reproduced below:

(a) In general. Each United States person having a financial interest in, or signature or other authority over, a bank, securities, or other financial account in a foreign country570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 13 shall report such relationship to the Commissioner of Internal Revenue for each year in which such relationship exists and shall provide such information as shall be specified in a reporting form prescribed under 31 U.S.C. 5314 to be filed by such persons. The form prescribed under section 5314 is the Report of Foreign Bank and Financial Accounts (TD—F 90-22.1), or any successor form. See paragraphs (g)(1) and (g)(2) of this section for a special rule for persons with a financial interest in 25 or more accounts, or signature or other authority over 25 or more accounts.

31 C.F.R. § 1010.350(a). Section 1010.350 then goes on to list and define the specific "reportable accounts" contained within the reporting requirement, including "bank account" "securities account," and other financial accounts. Id. § 1010.350(c)(1)-(4). It also defines the term "financial interest in a bank, securities or other financial account in a foreign country." Id. § 1010.350(e)(1)-(3).

8

There is also a "special rule" in the regulation for persons having a "financial interest in 25 or more foreign financial accounts"; per the regulation, those persons "need only provide the number of financial accounts and certain other basic information on the report, but will be required to provide detailed information concerning each account when so requested by the Secretary or his delegate." Id. § 1010.350(g).

570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1204 The second derives from Section 1010.306, entitled "Filing of reports," which further delineates these requirements as follows: (1) "[r]eports required to be filed by § 1010.350 shall be filed with FinCEN on or before June 30 of each calendar year with respect to foreign financial accounts exceeding $1,000 maintained during the previous calendar year," id. § 1010.306(c); (2) "[r]eports required570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 14 by . . . § 1010.350 . . . shall be filed on forms prescribed by the Secretary," id. § 1010.306(d); and (3) "[f]orms to be used in making the reports required by . . . § 1010.350 . . . may be obtained from BSA E-Filing System," id. § 1010.30(e).

The issue here is whether the term "violation" in 31 U.S.C. § 5321(a)(5)(A) is the failure to "file" a timely and accurate FBAR "form" or the failure to timely "report" the existence of a foreign transaction or foreign bank account. Under the former view urged by Solomon, her liability would be capped at $70,000—$10,000 for each of the seven years starting in 2004 through 2010. In her view, although she does not dispute that she maintained financial relationships with a total of twenty foreign accounts during those years and did not timely disclose those relationships, the violative conduct pertinent to calculating the applicable penalty is not the failure to disclose her interests in each of those foreign accounts but rather her failure to file a timely FBAR form during each calendar year. By contrast, the government argues that the violation as to which the IRS may impose a civil penalty is the failure to disclose the foreign account, and hence, that Solomon is liable for $200,000 because she did570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 15 not disclose a total of twenty foreign accounts maintained during the 2004-2010 period.

Upon a full review of the statutory and regulatory structure at issue, the latter view is most faithful to the statutory and regulatory text: the IRS is permitted to impose a civil penalty for a "violation," and a "violation" in this context is a failure to "report" a foreign transaction or bank account—not a failure to "file" an FBAR "form." Admittedly, there is some confusion stemming from the use of the terms "form" and "report" in the legal landscape, but as a review of the relevant provisions ultimately reveals, the FBAR "form" is simply the procedural mechanism by which the regulated person complies with her legal duty under § 5314 to "report" her interest in foreign bank accounts and transactions. It is that failure to timely "report" the underlying interest in the foreign bank account or transaction that constitutes the relevant "violation" for purposes of assessing penalties under § 5321—not the failure to "file" a FBAR "form." Here, Solomon committed 20 "violations" within the meaning of § 5321(a)(5)(A) when she failed to timely disclose the existence of twenty foreign bank accounts during the relevant period, and570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 16 hence the Secretary properly imposed $200,000 in total penalties for those violations (20 x $10,000).

To this end, the Court finds persuasive Judge Ikuta's dissent in United States v. Boyd, 991 F.3d 1077 (9th Cir. 2021) (Ikuta, J. dissenting) and hereby incorporates into this Order the reasoning in that dissenting opinion. A few key points are worth emphasizing.

First, the IRS may impose a penalty "on any person who violates, or causes any violation, of any provision of section 5314," 31 U.S.C. § 5321(5)(A), but the statute does not further define the term "violation," so we look to the substantive duty imposed in 31 U.S.C. § 5314. That statute 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1205 directs the Secretary to impose upon U.S. citizens/residents the duty to "keep records, file reports, or keep records and file reports, when the resident makes a transaction or maintains a relation for any person with a foreign financial agency." 31 U.S.C. § 5314(a) (emphases added). And then it mandates that such "records and reports" contain certain "information" as prescribed by the Secretary, including information about the "transaction or relationship" made or maintained by the U.S. resident/citizen. 31 U.S.C. § 5314(a)-(b) (addressing information that must be contained in the "records and reports," including information about the "transaction or relationship" and the parties/participants570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 17 to that transaction, and then permitting the Secretary to prescribe the "magnitude" and "kind[s]" of transactions subject to and/or exempt from Section 5314, among other matters).

Thus, while the language in 31 U.S.C. § 5314 refers to a citizen's requirement to "file reports," it is fundamentally focused on the citizen's substantive duty to disclose information about foreign financial transactions and financial relationships to the IRS. That is the core of the statutory duty imposed on citizens and residents. It is reinforced by the focus on "transactions" in the remainder of Section 5314, which requires the "records and reports" to contain "information" about the "participants in a transaction or relationship" and "a description of the transaction," 31 U.S.C. § 5314(a); see id. § 5314(b) (permitting Secretary to prescribe rules on the "magnitude" and "kind" of "transactions" subject to or exempted by Section 5314). And it is then carried out by directing the Secretary to prescribe the content of those reports and the manner of filing such reports, which the Secretary has done. See 31 C.F.R. §§ 1010.350, 1010.306. Put another way, what drives the citizen's duty in 31 U.S.C. § 5314—and what delineates the scope of the "violation" of that duty, see 31 U.S.C. § 5321(a)(5)(A)—is not the act of filing the report itself but rather the570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 18 obligation to disclose on the reporting form the citizen's foreign transactions and accounts. 31 U.S.C. § 5314.

Second, in keeping with the statutory duty to disclose financial relationships/transactions, the regulatory scheme as implemented draws a clear distinction between filing a reporting form, on the one hand, and reporting financial interests/relationships on those reporting forms. Section 1010.350—entitled "Reports of foreign financial accounts"—provides that each person "having a financial interest in . . . [a] financial account in a foreign country shall report such relationship to the Commissioner of Internal Revenue for each year in which such relationship exists and shall provide such information as shall be specified in a reporting form prescribed under 31 U.S.C. 5314 to be filed by such persons." See 31 C.F.R. § 1010.350(a) (emphases added). As that language indicates, the key is the reporting of foreign financial relationships to the IRS; the reporting form operates as the vehicle through which the citizen discloses the financial relationship to the IRS, but the requirement to submit a form to reflect that information does not alter the substantive nature of the underlying duty to report financial interests/relationships to the IRS.

Section 1010.306 continues570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 19 this distinction between reporting financial relationships/accounts on reporting forms versus filing forms themselves. It provides that "[r]eports required to be filed by § 1010.350 shall be filed with FinCEN on or before June 30 of each calendar year with respect to foreign financial accounts exceeding $10,000 maintained during the previous calendar year." 31 C.F.R. §1010.360(c) (emphases added). Then it provides that the "forms to be used in making the reports required by . . . 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1206 § 1010.350 shall be filed on forms prescribed by the Secretary." Id. § 1010.360(d) (emphasis added). And finally, it says that the "forms to be used in making the reports required by . . . § 1010.350 . . . may be obtained from BSA E-Filing System." 31 C.F.R. §1010.360(e) (emphases added). These provisions, like Section 1010.350, speak to two different things: the substantive duty to report the existence of financial accounts exceeding $10,000 during a calendar year, and the use of a form (the procedural mechanism) to carry out that substantive duty. Solomon's view that a "violation" is simply the failure to file a report essentially conflates these two concepts—minimizing the substantive duty to disclose financial interests, and ultimately transforming that substantive duty into more of a formalistic task of570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 20 filing a report.

Third, the regulatory scheme, viewed collectively, is geared explicitly toward transmitting information about financial interests in financial accounts and transactions to the IRS. We see this account-specific focus throughout 31 C.F.R. § 1010.350, which

(1) requires persons "having a financial interest in . . . a bank, securities, or other financial account in a foreign country" to "report such relationship . . . for each year in which such relationship exists," 31 C.F.R. § 1010.350(a) (emphasis added);

(2) details and defines the "[t]ypes of reportable accounts," including bank accounts, securities accounts, and other financial accounts, id. § 1010.350(c)(1)-(4) (emphasis added);

(3) further details the specific types of "[f]inancial interest[s]" in those accounts, id. § 1010.350(e)(1)-(3) (emphasis added);

(4) describes the specific types of "[s]ignature or other authority" that would give rise to a need to report the existence of those accounts, id. § 1010.350(f) (emphasis added); and

(5) permits persons with financial interests in 25 or more foreign accounts to identify, as a first step, only the number of foreign accounts on the FBAR form—but then expressly advises such persons that they "will be required to provide detailed information concerning each account when570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 21 so requested by the Secretary or his delegate." Id. § 1010.350(g) (emphasis added).

We also see this account-specific focus in Section 1010.420—entitled "Records to be made and retained by persons having financial interest in foreign financial accounts"—which operates in the same way, directing citizens to retain records about "financial interest[s]" in "accounts."

9

31 C.F.R. § 1010.420 ("Records of accounts required by § 1010.350 to be reported to the Commissioner of Internal Revenue shall be retained by each person having a financial interest in or signature or other authority over any such account. Such records shall contain the name in which each such account is maintained, the number or other designation of such account, the name and address of the foreign bank or other person with whom such account is maintained, the type of such account, and the maximum value of each such account during the reporting period.").

And that focus continues in the context of reports of transactions with foreign financial agencies and reports of coin and currency transactions. Id. §§ 1010.360, 1010.370.

This consistent emphasis on transactions and accounts—permeated in detail throughout the regulatory scheme—tracks the core substantive duty in Section 5314 to disclose information about foreign accounts and transactions to the IRS. Yet Solomon's view largely would minimize 570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 1207 that focus, elevating form (the filing of the FBAR form itself) over substance (reporting financial relationships) in a way that undermines the thrust of the statutory and regulatory scheme.

Fourth, there is the "reasonable cause" exception for non-willful violations in Section 5321(a)(5)(B)(ii). 31 U.S.C. § 5321(a)(5)(B)(ii). That exception provides that "[n]o penalty shall be imposed" for a non-willful violation of Section 5314 if "(I) such violation was due to reasonable cause, and (II) the amount of the transaction570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 22 or the balance in the account at the time of the transaction was properly reported." 31 U.S.C. § 5321(a)(5)(B)(ii). By its terms, this exception speaks in account-specific terms—not form-specific terms. Yet Solomon has provided no sensible way to make sense of that exception, or to evaluate how that exception applies, while simultaneously adopting her view that "violation" means simply a failure to file a FBAR report, regardless of the number of accounts that go unreported.

For all of these reasons, and for all of the reasons stated more ably by Judge Ikuta in the dissenting opinion in Boyd, it is the Court's view that Solomon's position fails as a matter of law. The term "violation" referenced in 31 U.S.C. § 5321(a)(5)(A) is not reducible to the procedural failure to file an FBAR form. Adopting such a view would undermine the statutory purpose of the reporting scheme, which is fundamentally about disclosing information to the IRS about foreign transactions and accounts. Instead, pursuant to the statutory duty imposed on U.S. citizens in Section 5314 and the implementing regulations, the plain meaning of the term "violation" in 31 U.S.C. § 5321(a)(5)(A) is the failure to report each foreign financial account on the FBAR form—not simply the failure to file the FBAR form itself.570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 23 Solomon committed twenty such "violations" in this case, thus authorizing the government's imposition of $200,000 in total penalties.

10

The Court acknowledges the contrary authority on this subject but respectfully reaches a different view.

CONCLUSION

For the foregoing reasons, it is hereby ORDERED AND ADJUDGED as follows:

1. Solomon's Motion for Partial Summary Judgment [ECF No. 11] is DENIED.

2. The Government's Cross-Motion for Partial Summary Judgment [ECF No. 19] is GRANTED.

3. Judgment in favor of the Government will be entered by separate order.

DONE AND ORDERED in Chambers at Fort Pierce, Florida this 27th day of October 2021.

FINAL JUDGMENT

THIS MATTER comes before the Court upon Defendant's Motion for Partial Summary Judgment (the "Motion") [ECF No. 11] and Plaintiff's Cross-Motion for Partial Summary Judgment (the "Cross-Motion") [ECF No. 19]. The Court denied Defendant's Motion and granted Plaintiff's Cross-Motion in a separate order [ECF No. 64]. In accordance with Federal Rule of Civil Procedure 58, the Court hereby

ORDERS and ADJUDGES as follows:

1. Judgment is entered in favor of Plaintiff United States and against Defendant Evelyn Solomon in the amount of $240,465.75 (inclusive of a late-payment penalty of $34,684.93, in addition to the FBAR penalty570 F. Supp. 3d 1195 2021 U.S. Dist. LEXIS 210602 2021 WL 5001911 at 24 assessment of $200,000.00, and pre-judgment interest of $5,780.82). Such prejudgment interest on the FBAR penalty assessment and late-payment penalties are provided for under 31 U.S.C. § 3717(a)(1) and 31 U.S.C. § 3717(e)(2) respectively. The prejudgment interest and late-payment penalties accrued from and after December 12, 2018, and to the date of entry of this judgment. Post-judgment interest on the FBAR penalty assessment shall accrue pursuant to 28 U.S.C. § 1961(a) and post-judgment late-payment penalties shall accrue pursuant to 31 U.S.C. § 3717(e)(2) and 31 C.F.R. §§ 5.5(a) and 901.9, until the judgment is paid in full.

2. The Clerk of Court is directed to CLOSE this case. Any pending motions are DENIED AS MOOT.

DONE AND ORDERED in Chambers at Fort Pierce, Florida this 1st day of November 2021.

End of Document